What are ESRS

Gli European Sustainability Reporting Standards (ESRS) are the European standards for sustainability reporting. Officially introduced by European Commission In July 2023, they represent the regulatory reference that defines methods, requirements and obligations with which companies must clearly and uniformly communicate their environmental, social and governance performance (ESG).

The ESRS are born within the European legislative framework for sustainability, in particular as an implementation of Corporate Sustainability Reporting Directive (CSRD), which came into force on January 5, 2023. This directive has updated and expanded the reporting obligations of non-financial information, requiring an increasing number of companies to report their ESG impacts according to comparable, transparent and verifiable criteria.

The standards were developed byEFRAG (European Financial Reporting Advisory Group) and are inspired by the main international references, such as GRI (Global Reporting Initiative), to promote a global convergence of reporting practices.

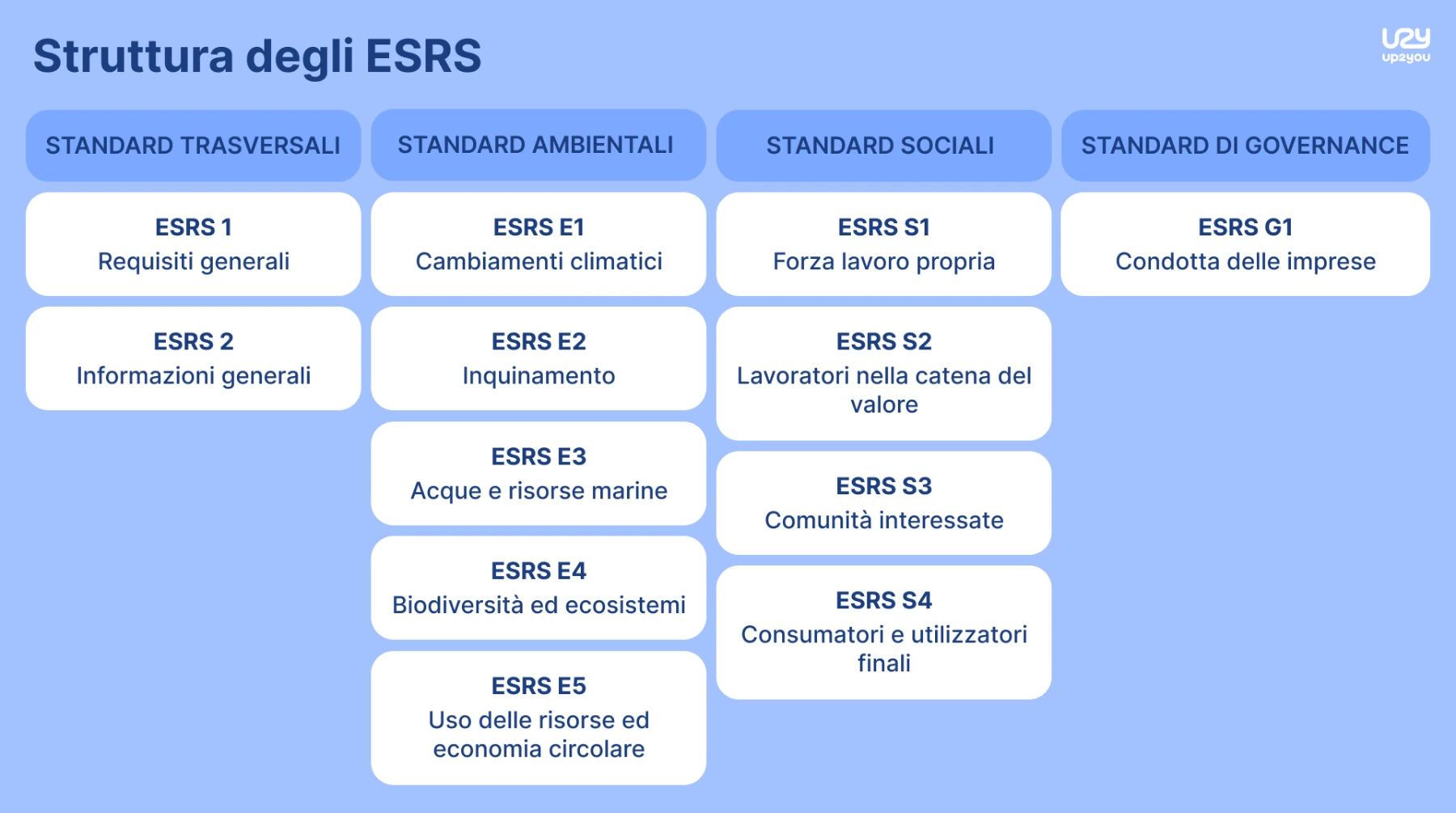

The ESRS regulatory set is composed of:

- 2 general standards, which define the principles and requirements that apply to all companies;

- 10 thematic standards, divided into five environmental, four social and one governance.

With ESRS, sustainability speaks a unique language throughout Europe, offering companies and stakeholders clear, comparable and reliable data on which Build strategic decisions.

Which companies do the ESRS apply to (and with what deadlines)

Gli ESRS apply to all companies subject to CSRD (Corporate Sustainability Reporting Directive), the legislation that introduced a new scope of reporting obligations on sustainability.

Not all companies, however, fall immediately under this obligation: the European Union has provided for a progressive extension over time, depending on the type and size of the companies, to allow aphased adoption of standards.

Let's see what the time frames are initially expected!

Wave 1: from January 1, 2024 (report for the 2024 financial year, publication 2025)

- Large companies already subject to the old NFRD directive

- Listed companies with more than 500 employees and at least one of the following conditions:

- Equity assets > 20 million euros

- Net revenues > 40 million euros

Wave 2: from January 1, 2025 (report on financial year 2025, publication 2026)

- All large unlisted companies that meet at least two of the following three criteria:

- capital assets > 25 million euros;

- net revenues > 50 million euros;

- average number of employees ≥ 250.

Wave 3: from January 1, 2026 (report on financial year 2026, publication 2027)

- Listed SMEs, subject to simplified standards, which meet at least two of the following criteria:

- capital assets > 450,000 euros;

- net revenues > 900,000 euros;

- average number of employees ≥ 10.

Wave 4: from January 1, 2028 (report for the financial year 2028, publication 2027)

- Non-EU companies with a significant presence in the European market, i.e. groups that:

- They generate at least 150 million euros of net revenues within the EU in the last two consecutive years;

- have at least one of the following characteristics:

- a subsidiary that meets CSRD dimensional requirements;

- a branch with net revenues > 40 million euros in the previous year.

Recently, with the regulatory package Omnibus, however, the so-called “Stop-the-Clock Directive”, which introduces important changes to the schedule for implementing the CSRD and the obligations related to the ESRS.

The main changes are:

- The 'Stop-the-Clock' is postponed by Two years the entry into force of reporting obligations for companies belonging to Wave 2 and Wave 3 of the CSRD;

- for Wave 2 (large unlisted companies) the obligation moves from 2025 to that 2027, with the first report in 2028;

- for Wave 3 (listed SMEs etc.) the obligation moves from the 2026 financial year to the year 2026 2028, with report in the 2029;

- The companies of Wave 1 are not subject to this delay: the deadlines already in force for 2024/2025 remain confirmed.

In addition, the Omnibus package also introduces proposals for simplifications of ESRS standards, to reduce administrative burdens and make the required information load clearer and more proportionate.

GRI vs ESRS Standards

Gli ESRS And the GRI standard represent two fundamental references for sustainability reporting, but they are born with different approaches and purposes.

I GRIS They were the first voluntary international framework widely adopted by companies globally to communicate their environmental, social and economic impacts in a transparent manner. Gli ESRS, on the other hand, are European standards of a binding nature, introduced by CSRD to make it mandatory to publish sustainability reports by subject companies, starting from 2025.

The main difference therefore concerns the regulatory force!

While the GRI remain one voluntary tool of reporting, ESRS are closely linked to a European directive And they involve legal obligations for businesses. In addition, the ESRS fully adopt the principle of double materiality, which requires us to consider not only theimpacting that a company generates on the environment and on society, but also the risks and opportunities what external factors entail for the company itself. The GRI, on the other hand, focus mainly on impactful materiality, that is, on the consequences of business activities towards the outside world.

Although born from different contexts, GRI and ESRS are, however, tracing a common route towards increasingly integrated reporting.

On September 4, 2023, EFRAG and GRI published a joint statement which confirms the high level of interoperability achieved. The definitions, concepts and criteria for the relevance of the impacts adopted by the ESRS largely coincide with those of the GRI, making reporting more consistent and reducing the risk of duplication.

For companies that already use GRI, this means a significant advantage: the information base is largely superimposable and constitutes a solid starting point for also fulfilling the obligations set out in the ESRS.

The dual materiality in ESRS

As anticipated, one of the most important conceptual pillars of ESRS It is the principle of double materiality.

Let's see more about what it is!

This approach requires businesses to assess the relevance of sustainability information from two complementary perspectives:

- impact materiality (external), concerns the effects that company activities have on the environment, society and human rights (CO2 emissions, use of natural resources, conditions of workers along the value chain, health and safety of communities);

- financial materiality (internal): considers how external factors related to sustainability can influence the economic value of the company, its financial performance and long-term resilience (risks deriving from climate change, new environmental regulations, social and reputational pressures, changes in raw material markets).

According to this principle, a sustainability issue is considered 'material' if relevant from at least one of the two perspectives, or both.

What are the ESRS provided for by EFRAG

Gli ESRS define in detail the information requirements that companies must provide regarding sustainability.

These standards pay particular attention to information Perspectives, that is, future-oriented, so as to evaluate not only Current performance of companies, but also the strength of their long-term sustainability strategies.

The overall picture consists of two transverse standards, valid for all topics, and from ten thematic standards, divided into the three ESG areas.

Cross-cutting standards

ESRS 1: General Requirements

It defines the general structure of sustainability reporting, establishing the basic principles and requirements for the preparation of reports.

ESRS 2: General Information

It establishes general information obligations, such as managing impacts, risks and opportunities, ensuring a minimum framework common to all companies.

Environmental standards

ESRS E1: Climate Change

Key standards for most businesses: concern mitigation and adaptation to climate change, energy consumption and related risks/opportunities.

ESRS E2: Pollution

It requires information on emissions and contamination of air, water, soil, microplastics and food resources.

ESRS E3: Water and Marine Resources

It covers water consumption and collection, water discharges, and the use of other marine resources.

ESRS E4: Biodiversity and Ecosystems

It focuses on business impacts on biodiversity, species loss, and ecosystem health.

ESRS E5: Resource Use and Circular Economy

It addresses inbound and outbound resource flows, the product lifecycle, waste management, and circular economy practices.

Social standards

ESRS S1: Own Workforce

It concerns working conditions, equal treatment, diversity, inclusion and equal opportunities for direct employees.

ESRS S2: Workers in the value chain

It focuses on rights, conditions and opportunities for indirect workers along the entire value chain.

ESRS S3: Affected Communities

Assess the impact of business activities on the rights and well-being of local communities.

ESRS S4: Consumers and End Users

It includes aspects related to security, privacy, accessibility and social inclusion of customers and end users.

Governance standards

ESRS G1: Business Conduct

It covers organizational culture and ethical principles: from political commitment to the fight against corruption, to animal welfare and whistleblowing mechanisms.